As discussed last week, Bitfinex has followed through with their bail-in and gave all of their users a 36% "haircut". While not ideal, with the right approach and conviction, this might be a way for the exchange to eventually right their customers. The idea is not new - I recall discussing something similar a few years ago when another big exchange was not measuring up...

MtGox's secondary market

MtGox, the poster child of why one shouldn't trust exchanges with one's BTC, has officially shut down in 2014. However, months before that you could already see some red flags popping up that something was going wrong. MtGox started having some fiat withdrawal problems, and as a result, its market was off by 10+% and ripe for arbitrage. Some people could make a tidy profit churning money around, provided they could get their fiat out of the exchange.

A few months later, the situation got worse - MtGox has officially halted both its bitcoin and fiat withdrawals altogether. However, probably due to some interesting code optimisation, someone figured out that if you withdraw bitcoins straight into a deposit address of another MtGox account, the funds would be transferred without creating a transaction on the blockchain. It looked like that functionality was governed by the "MOVE" API call, rather than "SEND". This tiny functionality was enough for someone to build an entire secondary market for MtGox before the whole exchange went under.

While I can't find any reference to what the site was (EDIT: the website was Bitcoin Builder, as pointed out by /u/samurai321), as the news of MtGox collapse has probably buried it in the sands of time, I remember it being a simple BTC-MtGoxBTC exchange. One could deposit actual bitcoins and trade them for bitcoins owed by MtGox that were moved to the secondary market's address. It allowed some people to get rid of their coins frozen at the exchange and cash out to the safety of the wallets their own, while letting others speculate on whether or not MtGox would be going under. I remember seeing the price reaching a level of 30+% discount on the market, which is fairly comparable to the current Bitfinex scenario...

Decentralised secondary markets

After MtGox collapsed, I haven't seen a similar secondary market pop up anywhere. The closest thing that comes to mind is being able to trade Bitstamp's IOUs on Ripple, which might be an ideal approach for trading exchanges' debt (at least provided the exchange doesn't run into new hacks). If Bitstamp was to go under, you could still trade about 1.5M USD and 2k BTC of its issue on the decentralised exchange nearly indefinitely. Figuring out its USD-USD and BTC-BTC exchange rate against an operating pool could be a clear gaige of confidence in the platform - if there were talks of the exchange recovering, the price might get closer to parity, or go away from it in the opposite case.

At the same time, such a secondary market might be used for something more morally muddy...

Buying one's own debt

Say Bitfinex's tokens were tradable during the hack. Before everyone knew how much was lost percentage-wise, the market would be wild with speculation - you probably could buy bitcoins at 50+% discount, perhaps even at 90% discount if the fear would set in. Now, if Bitfinex was aware of such a situation and knew how much deposits they could actually cover, they could try buying up their own debt for pennies on the dollar before the haircut was to take place. This could allow them to buy off some of their debt at a discount, reducing their obligations to their customers and therefore creating a theoretical profit.

Such a scenario would be highly unethical and I would guess highly illegal, but I wouldn't be surprised to see something like this happen sooner or later in the Bitcoin world. Instead, let's imagine some more ethical approach Bitfinex could act on their current situation...

Slow debt repayment

I'm not sure how Bitfinex structured their token program as I don't use the exchange. However, a good approach to eventually righting everyone would be for them to convert everyone's BTC balance into those tokens. At any time, the users would be able to cash the tokens in and get actual coins, minus the haircut. With each token converted, their obligations would decrease.

The tokens would also be tradable on the exchange itself for actual coins, creating a market for the debt. Anyone wishing to speculate would be able to trade the coins for a value between the haircut discount and 1BTC. The price would have upper and lower bounds, but could fluctuate in between.

If Bitfinex was diligent and set on repaying the debt by eventually buying up all of the tokens, they could publicly declare their strategy of doing so - perhaps a portion of their monthly income would go directly into purchasing the tokens from the market at the spot rate. With every purchase, the amount of tokens in circulation would decrease, thus the ratio of their bitcoins earmarked for buying back the tokens to the actual amount of tokens would increase, making the haircut smaller and smaller. Gradually, the gap between the value of the tokens and the real coins would shrink so much they could convert the tokens themselves straight into coins at a 1:1 ratio and remove them entirely.

In the end, the amount of coins you would get back would rely only on how quickly you need them - you could get them today for 36% off, perhaps get them for 30% off in a year, or get a full amount in a decade. The market would decide what the future value of the tokens would be, and with each month (and perhaps with each trade if some fees were to be maintained for this market), the debt would be slowly repaid.

In the end, this is an optimistic scenario assuming the exchange could earn back millions of dollars worth of coins before the company would go under. Similarly, if you believe the value of bitcoins will go up, the debt may never be repaid - the value of the coins left to be repaid could be going up as the number of the coins would be going down thanks to the increasing price.

One way or the other, it would be a really interesting case study if Bitfinex was to implement something like this...

This week, a high-profile Bitcoin theft took place at the Bitfinex exchange. The attacker reportedly stole 119'756BTC, worth about 70.5M USD. Those funds were held at a 2-out-of-3 multisignature wallet - one key was held at Bitfinex's server, another was kept by BitGo, and a third was a backup key held offline by Bitfinex. From what the reports say, the hacker was able to get their hands on the first key, as well as the API credentials required to authorise BitGo to process the withdrawal. With no additional safeguards, they were able to drain the hot wallet and land themselves around the number 2 spot of the biggest Bitcoin theft to date, after MtGox.

The scenario is still unfolding, so there are a lot of theories still floating around as to why the situation was allowed to take place. Some have speculated Bitfinex was forced to keep all of their coins in a hot wallet due to CFTC's ruling (as Bitfinex was not a registered futures trading platform), although it seems that the change was made before the ruling. Bitfinex also unveiled a plan for a "bail in", wherein everyone's assets would be devalued by about 36% so the exchange could continue operating.

Since Bitcoin's past seems to be littered with theft, I would like to have a look at one possible solution to minimise such high-profile hacks:

The way Voting Pools help secure users' funds is through shared responsibility from competing actors. Multiple exchanges of similar size would group together in a pool and secure one another's funds through multisig and a legal agreement to share responsibility in an event of a loss (be it from theft or one of the exchanges trying to run off with everyone's money). The multisig would be distributed in such a way that any one actor would not be able to control even their own money, and the system being robust enough to handle a loss of some keys (2-of-3, 3-of-5, 4-of-5, etc.).

This setup would make sure that a critical failure of one actor would not compromise the system. Even if one of the exchanges would burn down, get hacked, or the owner would decide to run away with all of the private keys, they couldn't do anything. The other exchanges would take over the responsibility and secure all of the funds to be able to pay all of the failed exchange's customers without suffering a loss of their own funds.

More importantly, however, this solution also forces every participating company to not only police themselves and ensure they have the most adequate security practices in place, but also to look at one another. When your own money is on the line, you will make sure everyone is keeping up with the rest of the pack in terms of keeping the money safe. Since the exchanges would still be competing with one another, they would have every incentive to expose other actors in the voting pool that are compromising the security.

Beyond that the full implementation of Voting Pools also necessitate that the exchanges would open up their transaction logs to one another to make sure everyone knows how much every customer is owed in case of a database wipe or the exchange vanishing from the face of the earth. This is pretty much automatic when it comes to gateways on a public ledger like Ripple or some shared permissioned blockchain, and it shouldn't be too hard to accomplish if an exchange already creates a strict and timely Proof of Solvency. That being said, it is pretty much unheard of for a normal Bitcoin exchange to do that currently, which might make it more problematic.

Having access to a full, real-time set of transaction logs the participants in a voting pool have everything they need to not only be able to settle with every customer in case the exchange goes under, but they can also police the exchange in real-time and raise flags in case of discrepancy. If exchange's liabilities exceed their assets, all withdrawals can be automatically haled until the matter is resolved. Large withdrawals, sudden market crashes and balance changes could similarly raise a lot of flags (to avoid another MtGox scenario, wherein a hacker crashed the market to be able to bypass the $1000/day withdraw limit).

Conclusions

All in all, voting pools would force a strong degree of transparency on every actor and couple that with multiple security teams making sure the system is secured against a growing number of hacks. While the participating exchanges would sacrifice their business data secrecy to their direct competitors, security through obscurity is never a good approach.

Leaving aside the discussion as to which approach would be the best for Bitcoin in the long run, we can agree that there is a disagreement on the issue and any hard fork that may happen will not be as unanimous as the previous forks were. Looking at some recent examples, we can expect that any contentious Bitcoin fork will create a split in the network.

Big players can trump forks - Elacoin

Last year Steve Sokolowski shared his thoughts on a Bitcoin hard fork proposal in a forum post. Other than discussing the actual solution, Steve also shared a story of Elacoin's attempted hard fork. Apparently, it was some unremarkable Proof of Work altcoin which activity has died off after awhile. A new developer came in and decided to breathe new life into the coin by creating a Proof-of-Stake fork. A lot of people got excited for the update and the trading volume and price rose back up.

When the fork was scheduled to take place, despite the backing of the community, the developers and stakers, the fork failed since Cryptsy continued to trade the coin without upgrading their daemon. Eventually the hard fork was deemed a failure while the old coins were still being traded.

This brings to mind the famous experiments with five monkeys, a ladder and a banana. People would trade a coin in anticipation of the fork, then ignore the fork and continue trading the coin due to its increased price and volume, completely forgetting why they were trading it in the first place. Classical altcoin speculators.

This only goes to show that big players, even if they are in a minority, can trump developer forks. While a story like this is rather unlikely to happen in Bitcoin, since the coin itself has many different markets and a vast community, we could experience a different problem when a hard fork happens...

New Coke vs Coke Classic - Ethereum

Not so long ago, Ethereum has experienced The DAO debacle, wherein a large quantity of ethers were drained from a high-profile smart contract. This prompted the Ethereum developers to create a hard fork that invalidated the attack. For a few days everything seemed to go smoothly - the majority of the network supported the fork, everyone transitioned just fine and it looked like the network could put the kerfuffle behind them. Then came Ethereum Classic...

Ethereum Classic is, I suppose, an "un-fork" of Ethereum - a codebase designed to ignore the DAO hard fork and continue the network as if it never happened. Whether the developers believe that they are supporting the community that disagrees with the fork, or they just want to make a quick buck, the fact is that the classic ethers (ETC) started being traded on Poloniex, probably one of the biggest altcoin exchanges currently, and now are being actively traded on a number of other exchanges with a current market cap of $200M and 24h trade volume of $65k - forth market cap after Bitcoin, Ethereum and Ripple, and having double the trading volume of Ethereum, second only to Bitcoin...

From a perspective of any Bitcoin core developer wanting to fork Bitcoin, this is probably the worst thing that could have happened in the given situation. Exchanges supporting both sides of a fork can set a precedent of what will happen when Bitcoin is forked in any fashion short of full unanimity. Even if the unforked version of Bitcoin has 1% of its market cap, that's $94M market waiting for an exchange to take their money - it would be the 7th largest coin market, around the halfway point between Litecoin and Dash.

As an Ethereum Developer pointed out in an Ethereum Foundation Skype Chat leak - ignoring Ethereum Classic means there is no money to be made, while embracing it allows you to tap into some "vestigial value remaining from the shared chain history".

Even if any potential fork has all of the support from all of the developers and miners, there isn't much one can do to stop the un-fork, perhaps short of a Coiledcoin-esque 51% attack. Even if networks like Ethereum implemented "the bomb" (a special smart contract that prints tokens out of thin air, intended to kill an un-forked network), a developer could just create another hard fork to disable that code pretty much like the DAO was disabled...

Kill it with fire

So when all is said and done, it looks like the only way to ensure only one version of Bitcoin is around, one would need to reach an overwhelming consensus with the developers, the miners and the exchanges to support only one part of the fork. Anything short of that will create a split network with duplicate tokens being created on both tines of the fork.

To ensure the rest of the network follows suit, someone should put aside some funds and mining power to be able to execute 51% attacks on any un-fork that would start being traded at an exchange. While a 51% attack in normal cases might be in the legal murky territory, perhaps using it to enforce a hard fork might not be seen as an attack on the currency, but as a part of the upgrade process. The law might not catch up to this conundrum for years still.

Conclusions

Anything short of an unanimous hard fork to Bitcoin will most likely result in a network split where both sides of the fork. The split will most likely be motivated by short-term profit to extract some remaining value from the alt-chain. A good way to ensure no such split happens would be to divert some resources to performing 51% attacks on the minority chain and thus causing whatever exchange that tries to trade them to lose money.

In the recent weeks there has been a resurgence of news about OneCoin, what appears to be a high-profile MLM ponzi scheme disguised as an altcoin. From what I can gather, the renewed popularity of the topic was sparked by OneCoin's Coin Rush Global Event:

Coin Rush Global Event

Watching this video as someone that has been around Bitcoin for 5 years now, there are more red flags here than you would see during International Workers' Day in some places. In fact, the video and OneCoin in general are such a good example of how you can bamboozle people by saying just the right thing that it might be a worthwhile exercise to dissect a lot of it.

The Basics

Going onto a cryptocurrency website you want to look for a few key pieces of information:

Who is developing the project / the code? You want to find at least a competent development team identifying themselves. Examples: Bitcoin, Ethereum, Ripple. For OneCoin, the best resource I could come across was OneDream Team's "Top Leaders", which only boasts some news.

Where is the company located? It is especially important for exchanges and other companies you're giving money to, but can be useful for the core development team if applicable. Examples: Ethereum (listed on the bottom page), Bitcoin Foundation, BitStamp, not as much for Bitcoin Core (as it's a more decentralised development) Ripple, OneCoin or xcoinx.

Where is the source code? If you can't see the code, you can't be sure what you're installing isn't malware or whether the blockchain itself is really there. Examples: Bitcoin, Ethereum, Ripple, but nothing for OneCoin.

Do any reputable exchanges trade it? A coin that isn't tradeable might not be a currency at all, but instead some "funny money". For a smorgasbord of examples, you can check out CoinMarketCap, indexing things as low as $8 market cap for COIN. OneCoin, despite boasting 5.2B USD market cap, is conspicuously missing...

Getting all five of the above points is a good start for any currency, but as we can see, even some of the largest coins are missing one or two of those features. Lacking all five does not bode well.

That's not how blockchain works

Putting all of that aside, let's look at the video proper and see what the event is about. Apparently the big news that day was that OneCoin is retiring it's old blockchain (!) and launching a new one in October so they can make more onecoins (!!). The justification being, and I kid you not, that they need more coins to grow, since there might not be enough coins for new merchants, Latin America, India, etc.

Let that sink in for a bit. A cryptocurrency that is not explicitly tied to a fiat currency is running out of coins for people. So instead of letting free market organically settle on a price it thinks the coins are worth and say, buying the coins from the market to give to the new merchants if they want, they instead decide to make more coins...

The issue is also more complicated than just that. OneCoin on its FAQ page claims its blockchain is mined with a custom solution based on Script and X11. However, you don't mine the blocks directly, instead "you just sign up on the mining dashboard on the exchange in your back office". This might remind some people of Proof of Stake or Delegated Proof of Stake, but no, OneCoin does it differently - "People are signed up and assigned to mining pools on a first come, first serve basis. Whenever a place is free you can join a pool.". The process appears to be:

You send OneCoin money to buy the right to mine the coin

You sign up to mine

You wait for your turn to mine

You get your coins

In other words, it's like purchasing coins from an exchange (send money, get coins), but with an arbitrary wait period (currently 3-6 MONTHS!) between sending money and receiving coins. As /u/TimTayshun pointed out, the block times are also very strange - too regular for a Bitcoin-like mining scheme. The blocks appear to be generated at the 10 minute mark without much variation. If there is any real mining going on, there is no real competition, no difficulty adjustment or anything like that. It looks a lot more like Ripple's Consensus algorithm than anything mining-related.

Splits and tokens

But even all of that is not the whole story. Enter the splits and tokens. You don't directly buy the onecoins, instead you buy packages that include tokens and splits:

Apparently in order to keep the price attractive, you split the tokens as you would company shares. In the end it means that you have a higher quantity of tokens that you can use for mining, but the value stays the same, I think. The splits apparently can only be used on the tokens, not the coins that are mined, and you can combo the various packages in some "strategy" to receive more and more splits.

This seems to accomplish a few things:

Make the process more opaque

Incentivise people to buy more and more packages to get the best value for their money

Make people feel like they are in control of how to get the most money and get ahead of everyone else

Widen the distance between real money and onecoins by extra few steps in a freemium-like model

So in other words, the entire system looks like a shady mobile app:

Because nothing inspires more confidence than a pyramid-like structure with the money flowing to the top...

There is also something about not actually purchasing tokens, but instead purchasing training from OneAcademy that conveniently comes with tokens, BVs and what have you, but at this point I think I made my point. Purchasing any cryptocurrency is simple - you take your money, you get your tokens. With OneCoin, a simple trade is a drawn out process taking many months with zero transparency. Mining is a joke, the numbers are multiplied over and over. But the story doesn't end there...

Show us your proof

During the Coin Rush Global Event, there have been a number of claims made about OneCoin and other coins as well. After hearing a lot of them, one feels the urge to shout "show us your proof". In no particular order:

OneCoin has 2 million active users, no other currency has as much - I would love to see a proof of that claim, since it not only asserts a lot of people are using OneCoin, but claims to know how many people are using other cryptocurrencies, which is an information that is hard to come by. Someone estimated Bitcoin to have 50M users by 2015, but that's a guess. How many people are actually active on Bitcoin or OneCoin, that would be interesting to know.

OneCoin has 4.5B USD market cap - seeing as the coins aren't actively traded at any reputable exchange and the blockchain is not verifiable, any number you throw out there is as valid as any other.

Bitcoin has almost no merchants taking it - there are 8000 physical locations taking Bitcoin today, in 2014 BitPay estimated the number to be over 20k. All in all, it would be interesting to see where the data is coming from, since it's not that easy to come by

OneCoin is in 195 countries, it's bigger than Western Union - It would be really interesting to see the actual list of their operations. There are 195 countries in the world, which means they would have to operate in the US, North Korea, Iran Sudan, Syria and Myanmar at the same time, violating a lot of international sanctions.

OneCoin can do more transactions than Visa and Mastercard combined - this would mean it can handle more than 2'000 transactions per second, it would be an impressive amount of data to synchronise in a blockchain

OneCoin stores all customer KYC information encrypted on the blockchain - this would not only be a huge customer data protection concern (blockchain by definition is shared between multiple parties, so all you need is a blockchain and encryption key leak and someone has compromised all of that data), but also an can be an issue of how decryption would be handled under a warrant

Even after pointing out the various problems for a long while, there is still a lot more that needs to be addressed. Going into detail on everything would probably make this lengthy article probably twice as long. So let's finish off everything else in some quicker fashion. What follows are various claims, quotes and other titbits from the video presentation:

It takes over a year to mine one bitcoin - unless you're 21.co, nobody advocates Bitcoin mining to newcomers. Just like mining gold in real life, it's best left to professional companies

There are "Mickey Mouse coins" that copy OneCoin's concept - don't flatter yourself, everyone is aping Bitcoin

Just like you need a driver's license to drive a car, you need a drivers license for the cryptocurrencies - one of the beautiful things about Bitcoin is that it's inclusive - anyone can use it, you don't need a permission. While education is valuable, forcing people to go through a test before they can use cryptos is missing the point

OneCoin wants to be number 1 cryptocurrency world-wide in 2 years

When Bitcoin was one year old, it was worth 15 cents and nobody cared about it - it took two years for Bitcoin to be worth 15 cents, but now the speed at which good coins accelerate in price has increased thanks to Bitcoin. Dissing on the history to make your coin appear better is a false equivalence

OneCoin is one year old and it already wrote history - not really, but it will certainly write history once the jig will be up

They are aiming to have 20 million active users and 1 million merchants in 2 years

"We are the bigger community - we decide what the philosophy of cryptocurrency is"

The merchant / Latin America / India market capitalization is X trillions, OneCoin is only worth 5 billion, it simply does not work - normal coin would allow the price to grow to accommodate the market and use the 8 decimal places the coin has. Saying that you need to increase the amount of coins to grow is like saying you need to slice an apple into more pieces to make it bigger

"We can close new registrations, reject merchants... Or make more coins!"

"Biggest coin out there is Ripplecoin [sic], with 100 billion coins[sic]", and OneCoin will increase its number of coins to 120 Billion to be bigger than Ripple - that will still make you 3 times smaller than Fedoracoin, why not go for more?

You can't increase the amount with the current blockchain, need to retire the blockchain and launch a "new, more powerful blockchain" - you could, if your developers were up to snuff. Or maybe you're doing this to delete some old data from the old blockchain, or introduce some different balances that aren't supposed to be there?

Every account balance will be doubled after the blockchain is updated - again, increasing the numbers is not the same as increasing the value those numbers represent

When posting a question "will my coins be worth less after the update", the answer is not a clear "yes or no", but instead saying that the value of coins comes from brand and usability

Restaurant or retail store will never take Bitcoin - 8000 times false

"OneCoin will write history, and the cryptocurrency comminuty will have to rewrite philosophy"

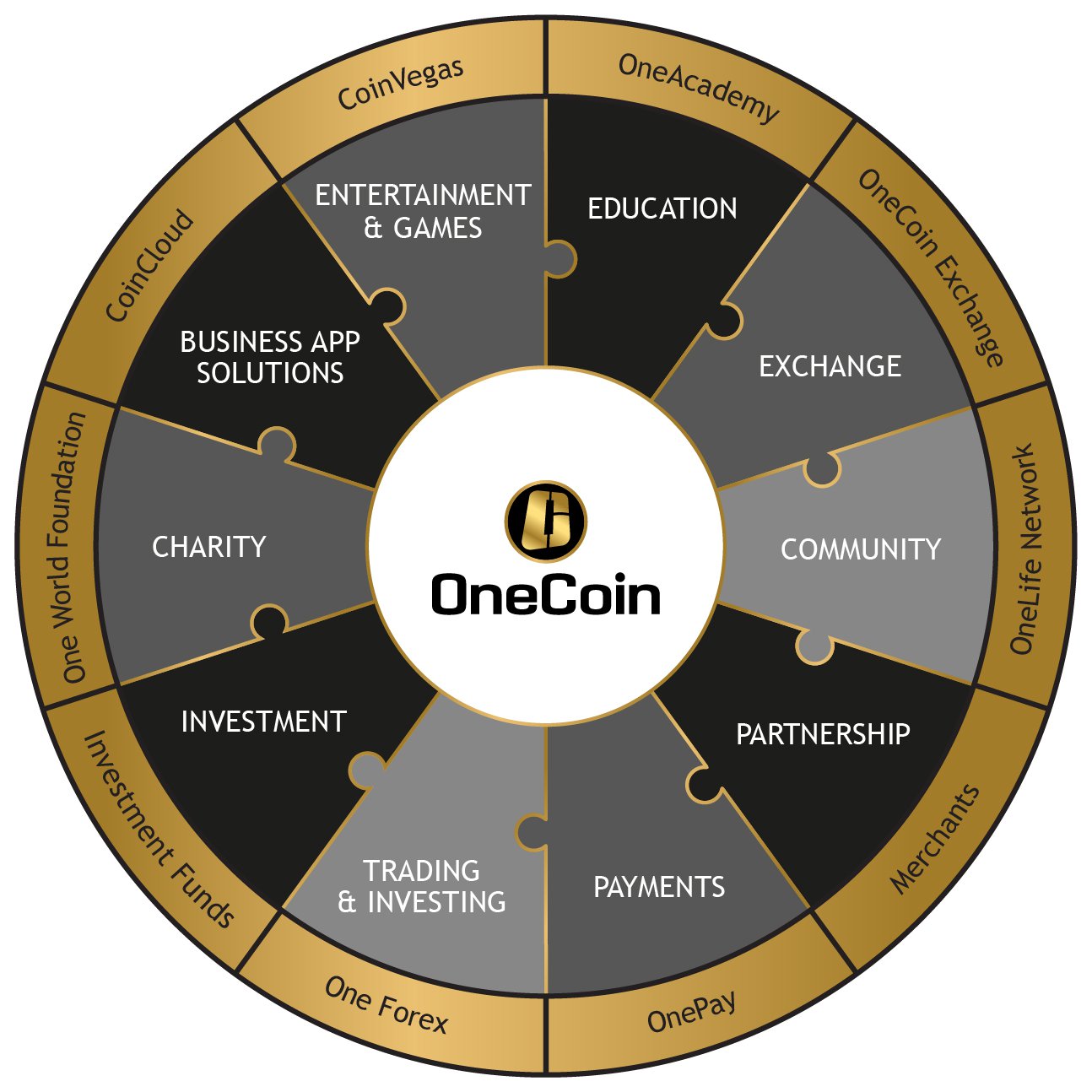

OneCoin, officially based in Dubai, boasts an impressive "ecosystem", consisting of 10 distinct items:

OneCoin's ecosystem

OneAcademy, an e-learning platform teaching about tarding, stock exchange, cryptocurrency, etc. in a 6-level program, boasting over 2'000'000 students and supporting 231 out of the current 195 world countries

OneExchange, currently not online

OneLife Network - "a digital platform with a unique ecosystem of sophisticated products and social networking tools that help members achieve financial independence", whatever that's supposed to mean. But fret not, they will offer you an "Ultimate Trader Package" for the low low price of 118'000 EUR, and a tablet to match for 550EUR, only 5-6 times more expensive than a comparable tablet. No contact information

CoinCloud - a cloud storage where you can buy 100GB of data space for 1 year for 3'030 EUR, which is about 1'500 times more expensive than Google Drive

There are 195-206 countries in the world. OneAcademy supports 231 of them

Conclusions

OneCoin, perhaps going in Microsoft's footsteps of wishing their products to be abbreviated into "The One" has raised a lot of red flags on all fronts. It does not instil any confidence in its products, its business strategy, or legitimacy of its creators. It takes money from a lot of people, turns it into a flashy show to boost confidence, and talks about its "community" and "family". The way it does business is overly complicated, intentionally opaque, and unverifiable. It is a blockchain and cryptocurrency only by self-proclamation. Keep as far away as you can from anything related and enjoy the slow-motion train wreck.

Your post advocates a new: (x) Altcoin (x) Permissioned blockchain (x) Centralised / decentralised exchange (x) Remittance service (x) Gambling website (x) Investment scheme (x) Wallet (x) Mining service (hardware, software, etc.) (x) Mining pool

Your idea will not work. Here is why it won't work.

(x) The proposed security model is (x) flawed / ( ) not enough / (x) completely wrong and therefore you will be ( ) scammed / ( ) hacked / ( ) stolen from / (x) implode quickly (x) There is already a product on the market that does exactly what you’re doing, but (x) faster / (x) cheaper / (x) better / (x) is more established / (x) is not a scam (x) You are proposing exorbitant fees for the use of your product that are unsustainable in the long run (x) Your product gives unfair preferential treatment to (x) yourself / (x) the earliest adopters / ( ) early investors / ( ) select few / ( ) _____________________ (x) You violate the core principles of Bitcoin, including: (x) core cryptography of the protocol / ( ) 21M coin limit / ( ) coin distribution / (x) ownership of private keys / (x) inclusive nature of the network / (x) pseudonymity of users / (x) lack of transaction censorship / ( ) ______________ (x) You promise unreasonable return on investment without a clear business model of where the money is coming from (x) Your project cannot be run legally at your jurisdiction (x) Your project will not be compliant with the current ( ) KYC / ( ) AML / (x) gambling / (x) MLM regulations (x) You rely on proprietary ( ) hardware / (x) software / ( ) intellectual property / ( ) _________ x) Your solution is worse than general-purpose computing hardware / software (x) Your product is poorly implemented (x) Your presale tokens have no economic value (x) Your adoption goals are unrealistic (x) Your product has zero transparency

Specifically, your plan fails to account for: (x) The existing regulations (x) The required Money Services Business license (x) The anonymous nature of cryptography (x) The geopolitical map of the world (x) Adaptability to growth of the market cap (x) The miner incentives (x) Public reluctance to accept weird new forms of money (x) Huge existing software and hardware investment in Bitcoin (x) The known security exploits of the existing Internet services (x) Secrecy of data decryption (x) Increase in currency unit supply not being the same thing as increase in wealth (x) Disproportionate increase in currency units drains wealth from one group into another (x) The long-term sustainability of the project

and the following philosophical objections may also apply: (x) It is a MLM scam (x) It is a pump and dump (x) It is a (x) ponzi / (x) pyramid / ( ) ___________ scheme (x) A known (x) scammer / (x) person with poor reputation is involved with your project (x) Why should we have to trust you and your servers? (x) Incompatibility with open source or open source licenses (x) Feel-good measures do nothing to solve the problem (x) Extraordinary claims require extraordinary evidence (aka “Proof or GTFO”) (x) I don’t trust YOU with the money

Furthermore, this is what I think about you: (x) Sorry dude, but I don't think it would work. (x) This is a stupid idea, and you're a stupid person for suggesting it. (x) You’re a scammer and you should feel bad.

Bitcoin Bullshit Tier You are advertising a new Bitcoin / crypto related project. Based on the information provided, you have reached the Bullshit Tier of 4 for the following reasons:

Bitcoin Bullshit Tier 1 - marketing babble, technology misunderstanding (x) “Blockchain” (x) “As good as / better than Bitcoin” (x) Misunderstanding the technology

Bitcoin Bullshit Tier 2 - willful misinformation, bait and switch (x) Selling overpriced / underperforming hardware or software (x) Claiming your project can accomplish something hard without a clear explanation of how to do so

Bitcoin Bullshit Tier 3 - Many red flags (x) Assuring your product is legal (x) Speaking about profits / return on investment (x) Providing no company contact information (x) Multiplying coins (x) Rebooting the blockchain (x) Company being hosted in hard to reach countries (x) Claiming your product services / is available at a large amount of institutions without a proof

Bitcoin Bullshit Tier 4 - Outright scams (x) High return on investment (x) Describing a financial security and claiming it’s not a security

DISCLAIMER: While I work for Factom, the opinions expressed in this piece are, as always, my own.

----

Working at Factom I came across an idea that seems seldom explored in the cryptocurrency space - a transactional currency called entry credits. They operate alongside the main currency of the network, factoids, but while factoids are a fully functional cryptocurrency that can freely circulate in the network, entry credits have a number of restrictions on them:

Entry credits are created out of factoids (by burning them) at an exchange rate dictated by the system, but they can't be turned back into factoids

Entry credits can be created ahead of time to lock in their factoid-entry credit exchange rate, and used later down the line

The exchange rate is tweaked by the system to stabilise the price of entry credits, while still allowing factoids to be a free-floating currency

Entry credits can only be spent (burned) to store entries into Factom - they can't be spent elsewhere

Entry credits are not transferable - they can only be spent by the account that received them during the factoid->entry credit conversion

These restrictions create a few interesting features for the system that I don't see explored much in other cryptocurrencies:

It is possible to put a large amount of entry credit tokens on a hot wallet without worrying much about theft - any would-be hacker wouldn't be able to cash out the stored value, only spend it. This makes production servers much less of a target for attacks.

Being able to lock in the price of the tokens ahead of time means companies can budget ahead of time and don't have to worry about token volatility

Having the exact amount of tokens in an account, one always knows how many transactions they can perform in the system before running out

Other tokens

While I haven't heard of another currency having the same features, there are some that function similarly.

Most cryptocurrencies adjust their transaction fees on a regular basis to keep up with the price of their coins. This can function as a way to keep the transaction cost stable without trying to control the price of a currency.

Ethereum uses a more formal approach to this with their gas currency. It is separate from their ethers, but you can't purchase gas ahead of time. The gas is used to pay for transactions and operations in smart contracts, but the final cost calculations are more complicated - one can get gas rebates for freeing up memory as far as I heard.

Conclusions

The Factom project might be one of the first projects to implement a fully transactional currency - entry credits. While being a confusing feature for some, it is an interesting approach of stabilising the transaction cost of production blockchain application, as well as limiting the attractiveness of an attack on the production servers.

If you hand around the Bitcoin space for awhile, you will inadvertently come across a few or a few hundredcopycoins, scamcoins, scams, ponzi schemes and what have you. Whether it's a large scam like Paycoin, small scale pump and dumps like Quarkcoin, or something that might look like an earnest project that got too big for its own good like The DAO, after awhile you start seeing the same pattern and red flags repeat themselves over and over again.

Being inspired by the ever timely SpamSolutions.txt (a quick checklist of "why your idea to solve the problem of spam won't work"), awhile back I started compiling "The Bitcoin Bullshit List" (also available at http://tiny.cc/Bullshit). It should be expansive enough to cover most of the common scenarios, but if you think it's missing something, let me know and I'll add it in the future revisions.

So, how does the Bitcoin Bullshit List work? You simply read up on or listen to a project pitch and start filling in the checkboxes in the "Your Crypto Idea Will Not Work" section. Once you're done, you can summarise your thoughts and give the project a short "Bitcoin Bullshit Tier".

Let's go through an example to show how this might work in practice (and cutting out the unnecessary parts of the lists).

Example - The DAO

Your post advocates a new: (x) Altcoin (x) Investment scheme

Your idea will not work. Here is why it won't work.

(x) Your target audience is too small to support the project (x) The proposed security model is (x) flawed / ( ) not enough / ( ) completely wrong and therefore you will be (x) scammed / (x) hacked / (x) stolen from / ( ) ________ quickly (x) You promise unreasonable return on investment without a clear business model of where the money is coming from (x) Your project cannot be run legally at your jurisdiction (x) Your project will not be compliant with the current (x) KYC / (x) AML / ( ) gambling / (x) securities regulations (x) The solution would work better as a (x) centralised / (x) decentralised / ( ) distributed solution (x) Your product is poorly implemented (x) Your presale tokens have no economic value (x) Your adoption goals are unrealistic

Specifically, your plan fails to account for: (x) The existing regulations (x) The required Money Services Business license (x) The anonymous nature of cryptography (x) Public reluctance to accept weird new forms of money (x) The human factor

and the following philosophical objections may also apply: (x) Ideas similar to yours are easy to come up with, yet none have ever been shown practical

Furthermore, this is what I think about you: (x) Sorry dude, but I don't think it would work.

Bitcoin Bullshit Tier You are advertising a new Bitcoin / crypto related project. Based on the information provided, you have reached the Bullshit Tier of 4 for the following reasons:

Bitcoin Bullshit Tier 1 - marketing babble, technology misunderstanding (x) Dropping names of crypto celebrities to bolster one’s credibility

Bitcoin Bullshit Tier 2 - willful misinformation, bait and switch (x) Claiming your project can accomplish something hard without a clear explanation of how to do so

Bitcoin Bullshit Tier 3 - Many red flags (x) Assuring your product is legal (x) Speaking about profits / return on investment (x) Presale (x) Token IPO (x) Providing no company contact information

Bitcoin Bullshit Tier 4 - Outright scams (x) Describing a financial security and claiming it’s not a security

Well, that was pretty straightforward. Now, let's compare that to something that is generally not considered a scam and see how well it fares.

Example - Litecoin

Your post advocates a new: (x) Altcoin

Your idea will not work. Here is why it won't work.

(x) There is already a product on the market that does exactly what you’re doing, but ( ) faster / ( ) cheaper / (x) better / (x) is more established / ( ) ______________ You are proposing exuberant fees for the use of your product that are unsustainable in the long run

Specifically, your plan fails to account for: (x) Public reluctance to accept weird new forms of money (x) Huge existing software and hardware investment in Bitcoin

and the following philosophical objections may also apply:

Furthermore, this is what I think about you: (x) Sorry dude, but I don't think it would work.

Bitcoin Bullshit Tier You are advertising a new Bitcoin / crypto related project. Based on the information provided, you have reached the Bullshit Tier of 1 for the following reasons:

Bitcoin Bullshit Tier 1 - marketing babble, technology misunderstanding (x) “As good as / better than Bitcoin”

Generally, not that bad - some tick boxes will apply to even the most benign and well meaning projects, and that's fine.

Conclusions

With many new crypto projects cropping up and vying for your money, it's useful to step back once in awhile and see how many flags certain projects raise before buying into them. Whether it's for laughs or as a sanity check, the Bitcoin Bullshit List might be a useful tool to run through when looking at new Bitcoin and crypto-related projects:

Last week marked a 100th post I have posted on this blog since about 2.5 years I've been blogging somewhat regularly. Today I would like to take a look back and do a bit of a retrospective on some things posted and an overall state of the blog.

General thoughts

Like most people, I get a lot of ideas on various subjects all of the time. Some are so-so, while others merit more contemplation. This is one of the reasons why I started writing this blog - to be able to formulate my thoughts, put them down somewhere and to be able to reference them later as needed - during online conversations, or when writing out other ideas.

It has really been a useful tool for me over the years - before I started writing the blog I would discuss some interesting ideas I had either without writing them down, or in random places over the Internet where I couldn't easily find them afterwards. This would usually mean I couldn't go into that much depth and the thoughts were more ephemeral.

A few months ago I was looking for some post on my blog and I stumbled upon the post about volatile currencies I have completely forgotten about at that point. It's perhaps not the most relevant or best written post out there, but it still contains an interesting idea nugget that might be a useful reference in the future. If I relied only on my memory, it would be gone.

With that in mind, lets look at some popular or interesting posts I have written over the years that you might've missed.

Top ten

Here are the ten most popular posts from this blog, based on the number of views:

Generally, not a bad cross-section of the blog - talking about Crypto 2.0s a number of times, criticising some projects that have some objectionable features, talking about some ideas I still wait to be implemented, etc. Some information is starting to get a bit outdated (I would've expanded the good list to include projects like Ethereum), but overall I can't complain.

Other good posts

The above posts got the most views. However, there are some other posts that I'm proud of. Maybe they got unlucky when they got posted, or the ideas presented are rather niche, but they might be still worth checking out:

Thank you everyone for sticking with me for the one hundred posts. If you find your mind similarly teeming with ideas, my advise to you would be to put them to writing. You may never know when your past self will surprise you with interesting thoughts that would otherwise flee.

Full disclosure - I own some ether and I have put some of it into The DAO presale. I don't think it coloured my view of the situation, but I feel it's better to be open about such things.

The DAO has made a lot of waves recently. First - last month when it became the largest crowdfunding project in history, at one point surpassing Star Citizen's 116M USD (although it might be partially due to ETH exchange rate fluctuations). Second time - earlier this week when the DAO was hacked. So lets start from the beginning and have a look at the rise and fall of The DAO.

DAOs, in general

DAO, or Decentralised Autonomous Organisations have been a fairly nebulous concept in the crypto space for awhile. They basically are computer programs that run as an organisation, using its code as law. They can hold digital assets and money that can be spend on various projects, services and other digital assets.

Of course, with the current level of cryptocurrency technology, the DAOs are very limited in scope. They can't be as sophisticated as modern AI running on supercomputers, and since code isn't lawfully binding - the various DAOs have to rely on humans to interface with the outside world.

TheDAO will create many jobs. First for people like me who have to explain what the hell it is.

The DAO

The DAO (holding a very generic "temporary name", which it probably won't escape from), created by Christoph Jentzsch, the founder of Slock.it, was set out to be one of such self-sustaining DAOs. It was set up to be a quasi-venture-capitalist-fund. As with many token crowdsales, it was skirting the borders of the law - allowing anyone to invest, not doing any KYC, promising "benefits to the DAO Token Holders", without outright selling securities.

The DAO started operations by selling its tokens for ETH. The promise was that later the ETH would be used to fund various projects and try to extract value from those projects to the DAO itself. The DAO also had a mechanism to upgrade itself to newer versions of the code. The entire process of both spending money and code upgrade would be governed by the token holders voting. Every vote would be proportional to the amount of tokens held.

By the end of the crowdsale, The DAO has raised 8.26M ETH, more than 10% of the total coin supply.

In theory, The DAO could've been a very strong player in the crypto space. Even if it would spend 10% of its funds just funding early stages companies, it could give out 100k USD to 100 different companies and probably have great ROI by the end.

As it turns out, The DAO had a small bug in it (discussion, technical overview). They managed to make a recursive call to a function and use that exploit to start draining The DAO of its ETH. Before the attack stopped, 3.6M ETH was extracted, worth about 50M USD give or take 20M due to wild price fluctuations.

The following day, we actually got a statement from "The Attacker" about the issue, claiming that the draining of ETH was legal and in accordance to The DAO's rules ("code is law", therefore any execution of the code is always as intended). The Attacker also threatens legal action against any attempt to freeze the drained ETH. If such a case ever made it into a court, it would probably be the most important precedent for the future of decentralised organisations as a whole. Only time will tell where the story goes.

Other criticism

If The DAO has not been taken down by this exploit, it is entirely possible we might've seen a lot of other problems crop up in the future. Here are just some of the possible issues and other ideas that would need to be considered.

Setting a precedent for Ethereum. The way Ethereum handles this exploit may affect how similar future problems would have to be addressed. If they go through with the blacklisting, they might be required by law or asked by the community to do the same in the future for a lot of other things. This can open up a big can of worms. However, if they don't, then they might scare off any other similar projects from using the platform, along with some of their users. Damned if you do, damned if you don't.

Voter apathy. If The DAO would have a large amount of users sitting idly on their tokens rather than voting with their money, the software might have problems reaching the needed quorum to do anything. Apparently in Bitshares, only about 10% of stakeholders participate in voting. Perhaps switching to a Delegated Voting model might help alleviate the issue.

Unexplored legal area. The DAO seems to have aimed to exist in an unexplored legal area. It operates like a security or a venture fund without doing the due diligence. It technically cannot be sued, but people that put money into it might face legal repercussions. All in all, it probably would give any lawyer and government official a headache to try framing it in the existing rule of law.

Lack of KYC. While a lot of people in the crypto community want the government and regulations as far from their projects as possible, some oversight might deter attackers. If every investor in The DAO would be vetted by KYC first, and if only vetted individuals could hold the tokens, anyone attacking The DAO would have to be prepared to get sued and criminally charged for their actions. Right now the best we've got is to try tracing the ETHs they owned back to an exchange and possibly investigate some Ethreum / DAO short calls someone might have set up before the attack (similarly to the idea of "terrorist insider trading").

Rushed deployment. After The DAO has been released, there have been some concerns from people that the code should've been tested and vetted more to iron out any bugs. A code that holds so much money is a gold-filled pinata for any and every hacker that might try to break it 24/7. Some attack vectors have been published before the attack (description and mitigation). Since the contract is vulnerable right after it's released, rushing a release is not wise.

Any bug needs to be fixed immediately. With a smart contract running on a decentralised network, it is vulnerable to exploits all the time. Any new bug that is found needs to be fixed right away, especially if it is described publicly. With more centralised software, you can at least shut everything down until the bug is fixed, but such luxury would be harder to implement in a DAO.

One mistake and your money is gone. While this one applies to most cryptocurrencies, it also bears mentioning - any bug in the code that breaks the smart contract that holds actual money (in this case, ETH) can cost you everything. If you deploy such a piece of code and send money to it, it is gone and you won't be able to get it back.

There are no rollbacks with real coins. While any contract that issues and deals only in its own tokens can be rolled back to any point in time with a patched contract, the matter is not as simple when we're dealing with actual coins (in this case, ETH). As the native coins exist outside of the contract's controls, using such contracts to manage the coins is more dangerous than just dealing in tokens.

Putting all eggs in one basket. A contract holding over 100M USD is a disaster waiting to happen. At the very least some of that money should've been put in some deep cold storage until it is needed. Enter into some legally binding contract with 50 people if you need to to provide some multisig and keep the funds safe. It's like putting all of your coins into a hot wallet - you shouldn't do that.

Paradox of presales. Even if The DAO would function correctly, it might be a hard value proposition, similar to most other ITOs (Initial Token Offering). Unless you are an actual security / fund and building projects that funnel their earnings into the organisation, the projects that benefit The DAO holders rather than Ethereum as a whole might be inferior to the general use case. There is a lot that the Ethereum platform and anything on it could benefit from, but tying them into one smart contract might defeat the purpose. Since many DAOs want to avoid being labelled as a security, we might just get some weird projects in the end.

Relation to other projects

A few people have started comparing this bug to a few other things in the cryptocurrency space. Perhaps it is important to have a look at them and figure out how similar they are.

In the early days of Bitcoin, in mid-2010, someone found a way to create 184'467'440'737.09551616 BTC (almost 10k times more coins than would ever exist) out of thin air in a so called "Value overflow incident". The bug was fixed and the network was rolled back. The bug is similar - use an unexpected way the code works to get access to more tokens than one should be able to. However, this situation is different as it breaks the core functionality of the entire network, rather than a sub-part of it that is not governed by the protocol. Rolling back the network to before the bug was introduced is entirely justified - it is something that shouldn't have happened. With The DAO, the situation is a bit different - the core network functioned as intended, it is the final product that was at fault.

Another incident similar to this was the fall of MtGox allegedly caused by Transaction Malleability, and the attack on JustCoin with Ripple's Partial Payment Flag. In both cases, the software creators did not anticipate an obscure network behaviour that lead to their downfall. In neither cases did the network got rolled back - it functioned as intended, and to my knowledge neither of those companies got bailed out for the bugs in their code. This would probably be the closest analogy.

The decision to bail the contract out and refund the drained ETH might be either seen as the Ethereum Foundation trying to mitigate the damage to the network's reputation, or it might be due to many of the Foundation members lending their credibility to the project itself. One way or the other, I doubt we would see many similar DAOs in the future with such lineup of big name supporters to mitigate any similar damage in the future.

What is also worth noting is that because of Bitcoin's success, a lot of the cryptocurrency projects may "suffer" from an accelerated growth. There have been many incidents in the earlier days of Bitcoin of people losing their money and it wasn't that big of a deal - the coins were worth only so much. However, with networks such as Ethereum being worth a billion dollars less than a year after release, you have similar high profile bugs, but the coins themselves are worth a lot more a lot quicker. Perhaps we should try stalling the gold rush until a project has been vetted by early adopters hammering out all of the kinks and best practices? It's probably not going to happen unfortunately...

Lastly, if the Tau developers want to brag about how their platform is / will be much better than Ethereum since such bugs can't happen there, it is your time to prove yourself - deliver us your implementation of The DAO in a language of your choice so we can pick it apart and see if it breaks.

Conclusions

The DAO has been an interesting ride. It allowed the ETH to double in value and crash back down. A project of this scope if executed correctly would certainly be a game changer for any cryptocurrency network. Unfortunately, as many have made this joke before, it seems The DAO was DOA (dead on arrival). With DAOs, it's perfection or bust.

Spells of Genesis card for The DAO, reading

"Holding so much energy, the Colossus is able to withstand all threats"...

As of the time of writing, we are less than 4'000 blocks / one month away from Bitcoin's second halvening (the 4-year block reward halving period). We are also in the middle of a price rally, rising from about 400 USD/BTC and currently going through the 650 USD/BTC price. This seems like a good a time as any to talk about some of my past experiences with Bitcoin rallies, bubbles, and the last halvening.

I joined the Bitcoin community during the rally for the First Bitcoin Bubble (or at least the first one everyone heard about). It is the little, insignificant blip on the chart above, but at the time it was the wild, uncharted territory. The price reached a staggering 30 USD/BTC (and as far as I remember, 40 USD/BTC equivalent on Bitomat). A lot of people, myself included, were getting into the Bitcoin mining fever, projecting to make astonishing amounts of money with their computers and GPUs. However, the bubble burst, MtGox got hacked and the future of Bitcoin was uncertain. Nothing like this has ever happened before, so we didn't know if the currency could recover from such a bubble, or was it all over. By November, bitcoins were trading for about 2.25 USD/BTC.

The 2012 Halvening

As it turns out, Bitcoin didn't die. The next year started a bit anaemic, at around 5 USD/BTC. The mining difficulty has died down after the mining fever and it looked like the price of $5 was a solid bottom where the miners would be earning about as much as they put in. The first halvening was a looming event, but we wouldn't see it until the end of that year. Early in the year I thought to myself that since $5 is a rather solid price for the miners to make a bit of money, after the halvening we should see the price be at least $10. Turns out I was right - after the event, which was rather uneventful, we did see the price in the teens. Good enough reason to go out and have a small Bitcoin party everyone seemed to have been organising for the occasion.

The Cyprus Bubble - early 2013

The early 2013 started strong - Bitcoin was growing rapidly from 25 USD/BTC to the high of over 250 USD/BTC. Some of it was driven by the starting ASIC hardware race, but I think the biggest event that contributed to the price was the Cyprus financial crisis and the bank deposit seizures / bail-ins. The bubble burst when MtGox halted its trading due to not being able to handle the market volumes. The price went down to under 60 USD/BTC as people were desperate to get rid of their BTC by any means necessary.

The China Bubble - late 2013

2013 saw not one, but two big bubbles. After Bitcoin was declared dead once more in October after Silk Road was shut down (after all, allegedly only drug traffickers use bitcoin!), Bitcoin started to show it can stand on its own and shed all of the bad press.

Around the same time Bitcoin was also heavily featured in the Money 2020 event with companies like Coinbase, BitPay and Blockchain representing (funny enough, this is what I saw at my hotel :) ).

However, despite those events being a definite boost to Bitcoin's price, it seems that the majority of the rally was done by people in China. Everyone seemed ecstatic about the price rally, posting pictures of moon landing after we reached 1000 USD/BTC, putting forward motions to switch from BTC to mBTC as a default denomination, etc. It was fun all around.

The rally ended similarly after Bitcoin was allegedly banned from Chinese banks. The price declined with some fluctuations, reaching a bottom of about 220 USD/BTC in February of 2014.

The fall of MtGox

MtGox was a mixed bag in Bitcoin's history. early on, it was the biggest exchange, they were even generous enough to bail out Bitomat after it lost its private keys. Heck, they even published an ad for Bitcoin in G8 Conference Magazine:

MtGox Bitcoin ad

However, after a few hacks and general incompetency, MtGox became a joke. Due to problems withdrawing fiat for awhile, the price on MtGox was consistently 10-15% higher than other exchanges (as everyone needed BTC to cash out). When Bitcoin withdrawals were shut down, someone set up a market for trading real BTC for MtGox BTC, since the site still allowed internal coin transfers. The price was going down below the market as the withdrawals stopped but the trading continued. Eventually, the exchange was shut down in early 2014 when Bitcoin was at its lowest since the last year's bubble.

The current situation

Currently, we seem to be in a middle of a next rally in preparation for the halvening. We started the year above 400 USD/BTC, and if the last halvening is to be believed, we should end it at at least 800 USD/BTC. However, it feels like a lot of people are rooting for a new all-time high. Well, only time will tell - Bitcoin is a honey badger, it does whatever it wants.

After speaking to Ohad Asor, the creator of Tau, about the below piece, it's apparently "blatant obvious nonsense about things [I] don't understand" and "the contradictions are all around. just like eth". The Tau presale was apparently also meant for "only well informed buyers", "i have morals. im not ethereum!".

So yeah, the Tau project is not for mere mortals like myself, and the spam and promotional videos are meant for intellectual elites that will then buy the exclusive tokens. The project looks much better suited for some high-end computer science academia really, but no, token presale is the way to go.

Disclaimer - the project appears to be delving really deep into the theoretical computer science that almost borders on philosophy. While I do have a masters degree in computer science, I can't claim I fully understand some of the topics Tau-Chain touches on or their implications. I will instead focus on more practical aspect of Tau and how it presents itself as a piece of software with practical use.

What is Tau-Chain?

So, what is Tau-Chain? Well, it's quite simple, just look at this graph from the founder of Tau:

A simple explanation of Tau-Chain...

Okay, it's not simple at all. This graph represents what sort of confusing things we're dealing with here...

Tau appears to be a new programming language, apparently similar to Idris. Unlike most traditional languages most programmers deal with on a daily basis, it is not turing-complete. Instead, it is a decidable programming language. What this means is that it avoids the halting problem, while still being able to do anything a finite turing machine can do. Since in practice we don't have infinite turing machines, from what I understand it should be able to do anything a turing-complete language could do. Apparently, this approach might be more secure. On top of that, Tau "has built-in P2P and blockchain".

Tau-Chain on the other hand, appears to be a sidechain-enabled blockchain that can run the Tau language. It seems to be similar to Ethereum with its contracts - both have a growing library of code embedded in it that anyone can call upon to build their code on. As I understand however, Ethereum's code can be more risky to use as you might not always be able to predict what the contract might do without its source code at hand, while Tau the language is more predictable in its execution?

The project also appears to have another component to it - the Agoras. As far as I can tell, they seem to be smart oracles that can execute various contracts and other Tau code. They appear to be able to interact with the Tau-Chain, as well as with one another directly. All in all, they remind me a lot of Codius, especially if you consider that that project aimed to be able to prove what code is being executed and so on. Not a bad feature, but there doesn't appear to be much new to talk about there.

What Tau-Chain promises

While initially researching Tau-Chain, one will stumble upon their promotional video:

Tau-Chain, solving all of your software development problems apparently...

Which lists a few outlandish claims about what Tau / Tau-Chain can deliver:

Software that always does what it is supposed to

No more bugs

Automatic requirement validation by the Tau client

It is impossible to write code that doesn't work

Thanks to Tau, the client doesn't need to trust the coder and vice versa

The payment for developing code is automatically paid when the code is verified by the Tau network

The Tau blockchain stores social norms, scientific theories, "whatever is based on facts and rules" (one example flashing in the video is "Once you start to eat you should never leave spoon, fork or knife on the table. Their place is on the plate.")

Tau-Chain code is reusable

Tau is a database of provably working code snippets

You can use the Tau-Chain to build search engines, social networks, market places

You can develop provable smart contracts on the Tau-Chain

As a software developer, I would take all of that with a huge grain of salt. Then again, it might be my turing-complete attitude talking and things might be different in the decidable language space. If this video was talking about traditional software languages, I would put my money on the video being about test-driven development - an approach to software development that starts with test cases (what the code should and should not do), and then developing the code to fulfil those tests. In theory this could mean that the software has no more bugs, it does what it is supposed to and can be verified automatically when new code is checked in. So while it would fulfil most of the listed requirements, in practice I would not expect it to be *the* solution to all problems - writing good test cases can be as hard and time consuming as writing good code, and I doubt 99% of the clients purchasing software would be able to use that. If the test cases aren't sufficiently complex, we might run into the problem of software being built just to tick the checkboxes and not much else. After all, any program operating on a sufficiently small domain could be replaced by a lookup table...

I am also very sceptical of how the software will decide what are the stored facts and how those will be handled and proven. Even more so when we're talking about "facts" about the real world and social norms. How do you prove you should not put used forks on the table, from a software perspective? How do you handle a problem having multiple contradictory answers (an infinite sum of (1-1+1-1...) can be proven to equal 0, 1, 0.5, -0.5, etc...)?

Some other claims I stumbled upon from other sources (1, 2, 3):

Tau client's behaviour is dictated on-chain, with the chain being able to hard-fork itself

Tau (-Chain?) has no rules at all, its users will set its behaviour

"Tau network will be able to download virtually the whole internet, practically giving everyone the same information Google has, and more: data can be queried and processed more meaningfully and collaboratively, so you could perform queries as you like."

While there are more claims, lets just limit ourselves to those few (a lot more can be found in the LTB interview).

The Tau / Tau-Chain's feature of embedding how the network operates in the blocks themselves is rather unique feature as far as blockchains go, but at the same time it can be one of the more dangerous thing out there. It certainly offers the network more apparent freedom from Bitcoin-like hardfork stalemate, although in reality Bitcoin's hardfork problems are never about the code being hard to change, but about the people you need to convince. It might also impair some thin clients if they are applicable to the chain (how can you just run the chain from a given length if you don't know what the rules are from all of the previous blocks?). The definition of who the "users" in the system are (one-vote-per-person / machine / CPU?), as well as what the rules for hard-forks will be will probably shape the network very drastically early on. I wonder whether anyone will try to change the code of how the blocks are executed to "stop execution, return 0"...

The token presale doesn't appear to be anything new in the crypto world - it's the paradox of presales all over again. Tau the language and network doesn't need a new coin, it would probably operate better without it, but the developers need money to develop the language / network, so they sell tokens to speculators. Looks to me like another Bob Surplus-esque coin looking for a problem.

As for the last claim, and a few similar marketing blurbs, I think they deserve a section all of their own...

False equivalence, false dichotomy, eating your own dog food

The quote about basically being able to replace Google appears to be a false equivalence fallacy. There are many problems with trying to say you can basically be like Google:

Google is as much about the data (what the websites contain), as much as it is about the metadata (what the people are searching for and what they are clicking). Having just one part of that might not give you the full picture

Without having most of the data at hand, it is impossible to know if you returned most of the searched data. While you might be able to make queries based on the data you do know, you can never know how much you don't know

It is also impossible to prove that real-world data is correct. Since Tau-Chain is focused on storing "whatever is based on facts and rules", how would you be able to know, say, what is the weather outside right now? Sure, you can have a lot of data points, but you can't prove they are true or made up

All in all, statements like that are just red flags if someone also asks you for money. At best, they are marketing superlatives. So while sure, if we're talking about Tau the language, someone might use it to implement a Google-like service with it and so on, but the same could be said about computers based on cogs and wheels (after all, any turing machine is equivalent to another). All in all - false equivalence - your software is not even comparable to Google.

Now, lets finish this discussion with a subtle false dichotomy. I stumbled upon this marketing blurb about Tau from some of the spam I see pasted in a few chats I visit:

It compares how Tau-Chain is different from Ethereum, and links to a blog post by Peter Vessenes criticising how buggy some of the Ethereum smart contracts can be. He makes a lot of valid points - since you can't upgrade and fix the contract code post-launch, you either need a good failsafe, or write perfect code not to lose people's money. However, what I take slight annoyance with, is how this sort of marketing might misrepresent the situation - "Tau is different from Ethereum, here are a few reasons why. Here is someone criticising Ethereum (while not talking about Tau)", implying that since Tau was not criticised and it is presented as Ethereum's competitor, it somehow doesn't have those flaws. No Tau, criticism of your competitor does not mean you don't / won't have those problems yourself.

Lastly, I find it really amusing that Tau apparently doesn't like the taste of its own dog food - for all of its criticism of turing-complete languages, saying how Tau is a much better language and all of that, in the end they develop their code in C++. I did bring this point up to Tau's creator and he made valid points as to why that is - they want to develop the software in an efficient language to make it operate efficiently and in the future they might implement Tau-Chain in Tau. Understandably, software development takes a lot of resources and time, and you want to release early, release often, but this somehow doesn't fill me with confidence that Tau will be usable for any commercial-grade software any time soon...

Conclusions

While Tau appears to be an interesting development of a new programming language and its creator certainly sounds very knowledgeable in his field, Tau-Chain looks like a project looking for a problem. Bootstrapping a new token to run a blockchain to use a new programming language for smart contracts that don't halt seems like a very complicated way of reinventing everything just because you want to change a few things. I am highly sceptical of how the network will handle everything it promises, especially when it comes to dealing with things in the real world. It could be as mundane as a different flavour of Ethereum with a non-turing complete language, some smart oracles, etc., or something potentially new - only time will tell. Until Tau-Chain is released, I remain unconvinced.

Amusingly enough, the Tau-Chain video contains an Escher-like perpetual motion water mill at 1:40. I wonder if this is telling that the project is trying to invent something impossible?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}